Hurricanes, High Winds and Homeowners’ Insurance

Hurricanes, High Winds and Homeowners’ Insurance

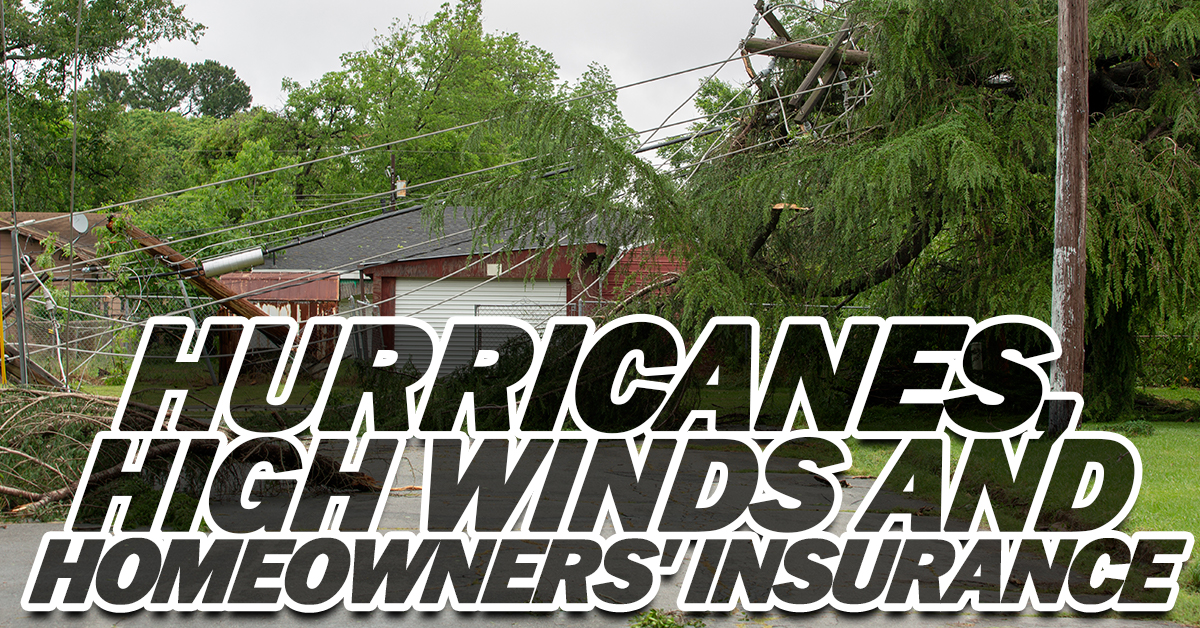

Winds come in a variety of forms. There are tornadoes, straight line winds, ‘Noreasters and hurricanes. The good news is that if high winds should damage your home, your homeowners’ insurance policy will likely cover the damage. This usually includes damage to roofs and siding as well as damage done from fallen trees. Winds are, in fact, one of the biggest factors that cause homeowners to file homeowners’ insurance claims. Depending on where you call home, you may experience a variety of winds during any given year.

The Midwest is known for the strength of its tornadoes, rated on the Fujita scale. An F0 tornado, known as a Gale tornado, ranges from 40-72 miles per hour. An F3 or Severe Tornado has winds ranging from 158-206. An F5 or Incredible Tornado has winds that range from 262-318 mph. Florida, known for its number of tornadoes generally has less severe twisters.

When it comes to hurricanes, winds must reach 74 miles per hour to become a level one. Level 2 hurricanes start at 96 miles per hour. Strong hurricanes begin at 111 miles per hour with Category 4 storms rated at 130 mph. Hurricanes reaching 157 mph or more are considered powerful Category 5 storms.

High winds, however, do not need to be accompanied by a tornado or hurricane to do damage. Winds as low as 40-60 mph can have damaging winds, much of it caused by blowing debris and falling limbs. High winds in especially wet conditions can be particularly damaging do to uprooted root systems. Tree damage can also be severe in areas that haven’t experienced high winds over several years. It is a form of Mother Nature’s trimming services.

If you are unsure of your homeowners’ insurance coverage or what wind-related coverage you may have, contact one of our independent insurance agents. They’ll review your current policy and seek out quotes that could potentially save you money. Get the peace of mind you deserve in high winds by contacting us today. We look forward to assisting you.

Do you have questions about your insurance? Find an insurance agent near you with our Agent Finder

Search All Blogs

Read More Blogs

From “Gruntled” Workers to Cyber Resilience: Protecting Your Team

Happy Gruntled Workers Day! A happy team is your best security asset. Learn why protecting your business from internal and external digital threats is the hallmark of a resilient leader.

Beyond the Policy: Life Insurance as an Intergenerational Wealth Engine

Financial freedom isn’t just for you—it’s for your future generations. Discover how permanent life insurance serves as the ultimate wealth-transfer tool.

Shark Week on the Highway: Avoiding “Predatory” Road Hazards

Shark Week is here! Learn how to spot “predatory” road hazards and keep your driving record clean this summer.

Beyond the Barbecue: Your July “Mid-Summer Maintenance” Checklist

Don’t let summer heat ruin your home. A quick mid-July maintenance audit can prevent major claims and keep your insurance premiums stable.

The Boycott of July 4th: Uncovering the Forgotten Quirks of Independence Day

Think you know the history of Independence Day? Discover why a Founding Father boycotted July 4th and the mind-blowing coincidences behind the holiday.

The Supply Chain Surge: Protecting Your Operations During the Holiday Rush

Summer demand is peaking, and deliveries are in overdrive. Learn how to protect your fleet, your cargo, and your bottom line from costly seasonal logistics claims.

Red, White, and Protected: Your 4th of July Backyard Liability Blueprint

Is your backyard ready for the 4th of July crowds? Learn how to protect your guests and your assets with a mid-summer home insurance safety check.

From Great Fires to Digital Twinning: The Story of Insurance Awareness Day

Why do we celebrate insurance on June 28? Discover the fiery history of this holiday and the world’s most “Bizarre” insurance policies.